Forecast portfolio risk with precision and manage exposures confidently with a foundation model purpose-built for tabular data.

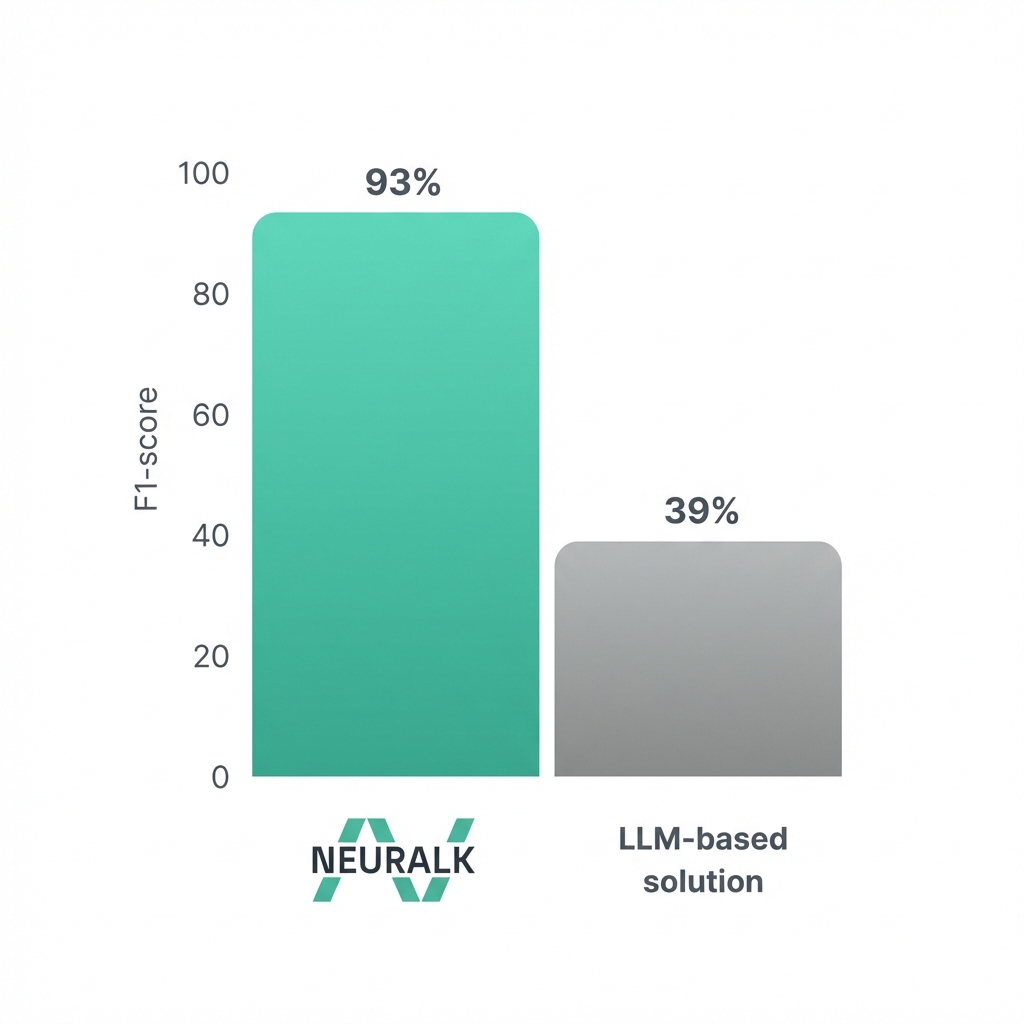

Our NICL Tabular Foundation model forecasts at state-of-the-art accuracy, outperforming traditional econometric models like GARCH, DCC, and shrinkage estimators, all while skipping the overhead of traditional model calibration, parameter tuning, and model maintenance.

Leverage a single foundational model for multiple forecasting use cases and simulations, from dynamic hedging to Stress testing and predicting tail losses under hypothetical market scenarios. Better accuracy, lower maintenance costs, and the guarantee of State-of-the-Art improvements from our research team.

Pretrained on millions of synthetic datasets, our predictive models have learned the complex patterns and correlations hidden within market microstructure, fundamental ratios, alternative data, and time-series features — out-of-the-box.

This deep understanding of tabular data enables our Predictive Foundational models to outperform both traditional ML models and LLMs.

Unlocking Predictive AI for your structured data